Recent performance and volatility of the MSCI World Index exhibits this.

The MSCI World Index

The MSCI World Index is a market capitalisation weighted index, the constituents’ weights fluctuate as their market weights fluctuate. In other words, as a share trades at a higher price, their market capitalisation increases, leading to them representing a larger portion of the index. This is not necessarily a problem if the share is fairly valued and re-rating; but in the instance where it is overvalued, it further inflates the valuation. This problem is exacerbated by passive investors who continue to purchase these companies to maintain their weight in an index tracking portfolio, pushing the price (and weight) up even further.

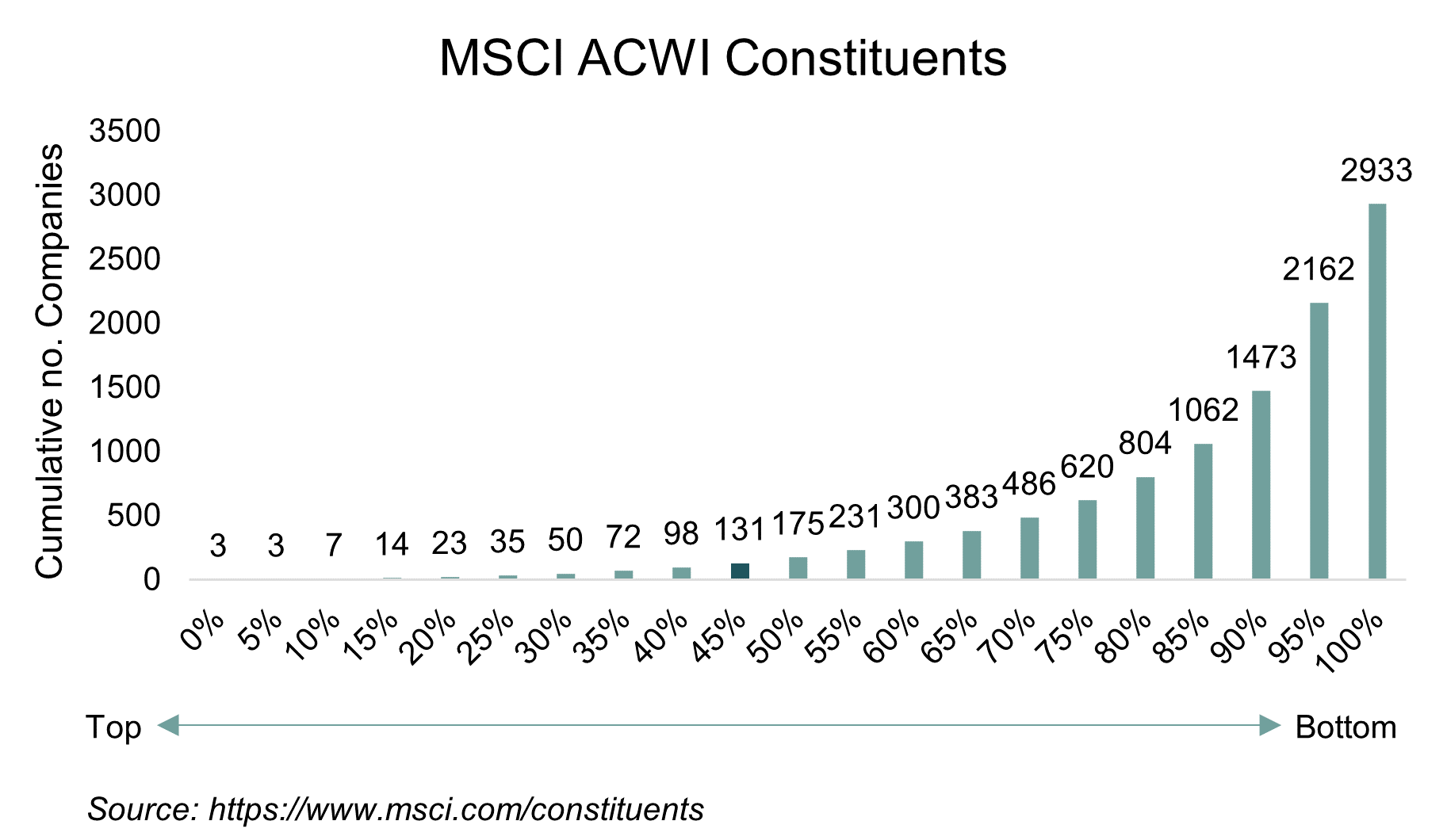

Although there are almost 3,000 constituents in the index, 50% of the index’s value is determined by only 131 companies. In other words, half of the index’s value is influenced by the performance of less than 5% of the constituents. This is exhibited in the graph below. Three companies make up 5% of the index, seven make up 15%, fourteen 20% and so on.

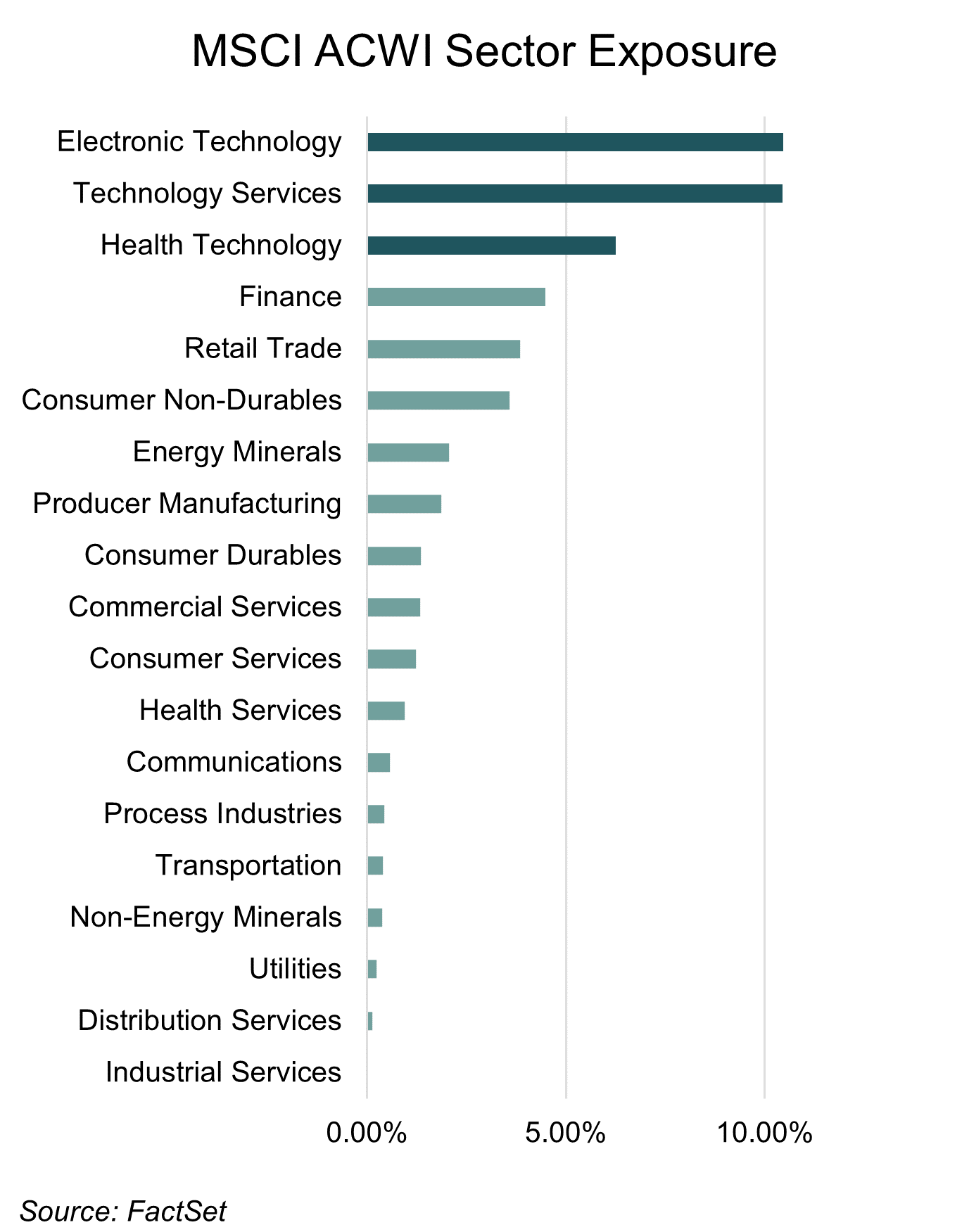

If we analyse the sector composition of the 131 shares that represent 50% of the value of the index in terms of sector composition, around 30% sits in technology and technology related companies.

In terms of effective risk management, one would not invest half of their portfolio in 5% of the constituents or one sector. This would lead to concentration risk and inflate the overall volatility of the portfolio. The MSCI World Index has almost 3,000 constituents, in the average segregated portfolio of 30 to 40 shares, this would equate to investing half of your capital in just 1 to 2 shares.

Although the index represents 99% of the investible global equity market, it is highly concentrated. A diversified portfolio exhibits far less volatility than a concentrated one. Lower volatility translates into smoother returns for investors. In a concentrated portfolio, price movement within the heavily weighted constituents or sectors will dominate returns. While this may be an attractive investment opportunity while the sector is appreciating, the potential downside should not be ignored.

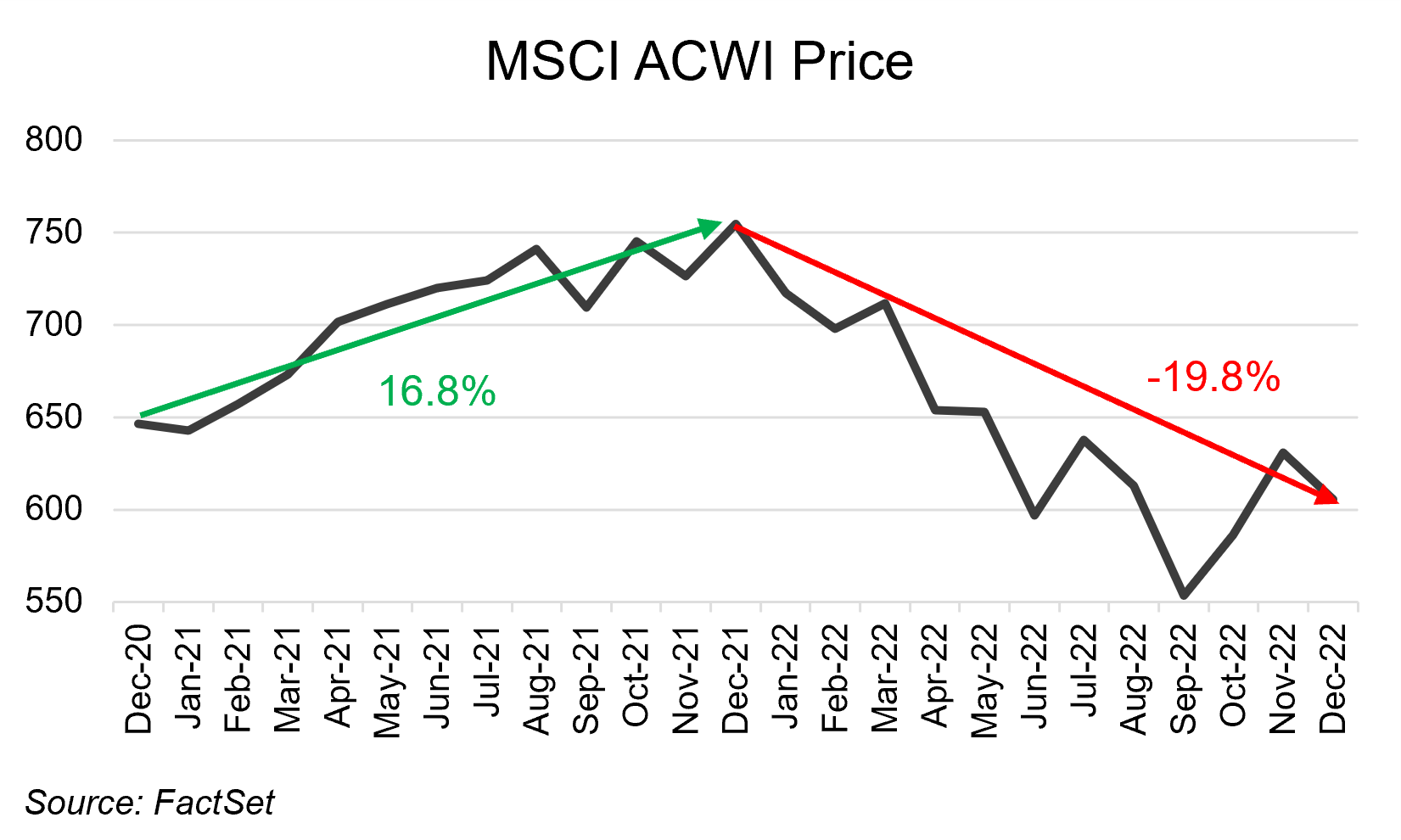

Performance over the 2021 and 2022 calendar years illustrates this concept. 2021 was a positive year for the index, appreciating 16.8%. 2022 however, saw a 19.8% decline.

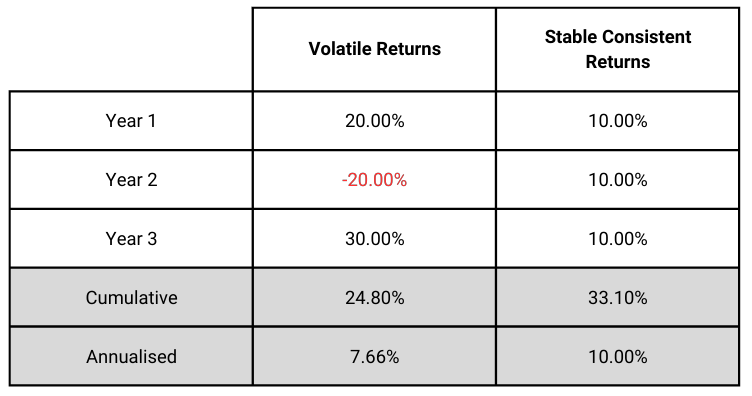

Although within a diversified portfolio you may not experience the same inflated returns delivered by the prevailing top index performers, your experienced drawdowns will also be muted. A simple calculation shows the impact of volatility on returns, when compared to stable, consistent returns.

Although the volatile returns in years 1 and 3 were higher than the stable returns, the stable returns were higher over the full period and delivered a more consistent return.

As part of the investment process and resultant portfolio construction, the valuation of a holding is analysed. One of the requirements is that the asset must be priced appropriately. Assets can be value additive if they pay dividends or appreciate in value, or both. If one purchases an asset at a premium, it necessitates higher compensation – either in the form of income or growth.

When assets trade at high valuations compared to their own history or the industry in which they operate, they are relatively overvalued and the risk lies in them de-rating back to normalised levels. This often happens when investors have overestimated their potential growth.

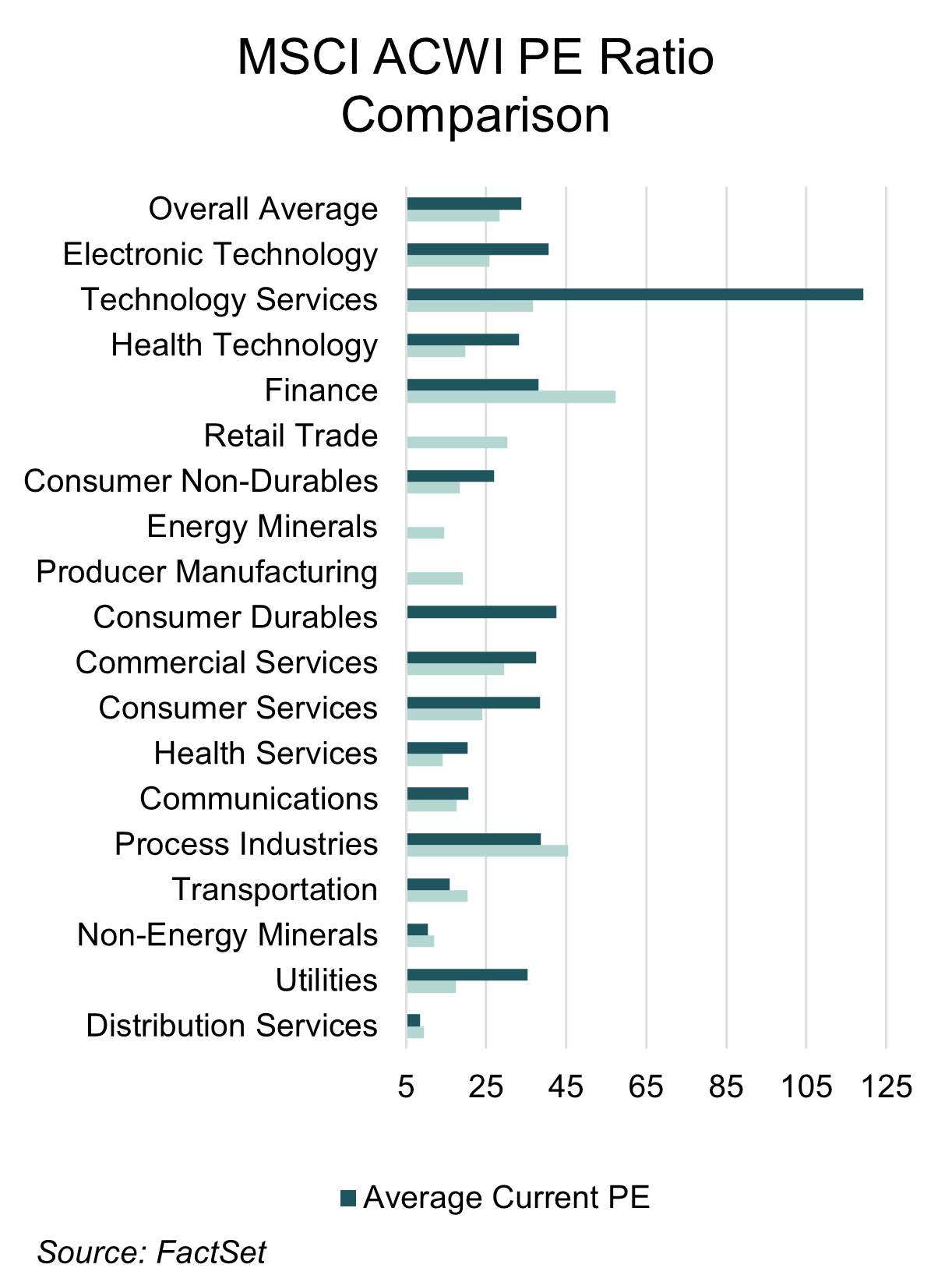

Below is a comparison of the average historical PE ratios of the top 50% of the MSCI World Index’s constituents as well as their current PE ratios. It is additionally important to note that an earnings yield has been used to calculate historical PE ratios to account for years of negative earnings.

1 Comment

Comments are closed.